When Cass entered adulthood, she had the same expectation as many Canadians before her: work hard, save steadily and one day buy a home. By her mid-30s, however, home ownership felt increasingly out of reach, even in Alberta—long considered a comparatively accessible market.

Cass and her husband, Mike, first looked to buy in Calgary in 2016, when they were in their early 30s. Back then, the market seemed manageable. Sales had dipped, prices had softened, and throughout that year the city’s overall benchmark price hovered just above $400,000. Then Mike went back to school for specialty healthcare training, and they hit pause on their plans. It made sense to keep renting and use the money they’d been saving for a down payment for the five-year program’s tuition instead.

Five years later, in 2021, the housing market shifted dramatically. Home prices across the country began rising midway through 2020, driven in part by historically low borrowing costs and changing demand for space as remote work became more common. Calgary logged a record year for home sales in 2021, with the benchmark price ending the year at over $464,000. As prices climbed, many millennials like Cass found it harder to get a foothold in the market. Existing homeowners, meanwhile, saw their properties evolve from just places to live into financial windfalls rapidly increasing in value. While these weren’t Vancouver or Toronto prices, housing affordability was starting to affect almost everyone in Canada, including Albertans.

Municipal leaders were blunt about the situation. “Calgary is in a housing crisis,” begins the City of Calgary’s housing strategy. Approved in 2023 and set to run through 2030, it’s a 98-action plan to increase supply and affordability. Nearly one in five households cannot afford their housing, the strategy states, and with costs continuing to rise, “more Calgarians are seeing their dreams of homeownership becoming further out of reach.”

That was the case for Cass and Mike. Their subsequent years of renting, and their eventual search again for a home to buy, were shaped by policies at every level—from federal programs such as the new First Home Savings Account, to the provincial affordable housing strategy, to municipal zoning rules that affect what is available and where. Their experience offers a window into how governments are trying to make homeownership attainable for first-time buyers, in a market very different from the one encountered by Canadians before them. They continued to rent, including an apartment in Calgary and a house in Cochrane, which they eventually had to leave in 2020 when the landlords decided to move back in. Between places, they lived with Cass’s parents, a stopgap she acknowledges not everyone has available or would enjoy. “We all like each other,” she says. “We’re very fortunate.”

Next they felt settled renting a three-bedroom house in the northwest Calgary community of Dalhousie, but their rent rose, from $1,750 in 2020 to $2,800 in 2024—and then the landlord decided to sell. Renting felt increasingly precarious, Cass says, especially in a province without rent control or any prospect of additional protections for renters. In 2025, for instance, a provincial government spokesperson told The Globe and Mail “Alberta will not go down the disastrous road of rent control.”

With rents roughly equal to a mortgage payment and Cass and Mike both feeling more settled in their careers—she as a manager at an architecture firm, he practising manual osteopathy—they decided it was time to again consider buying. They began watching listings in late 2024 as Calgary’s benchmark price neared $588,000, with supply tight as more and more people poured into the city.

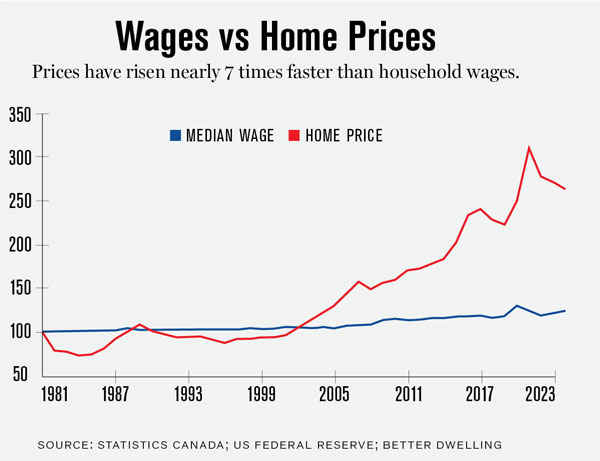

Housing affordability, meanwhile, had become a defining national issue as several forces converged. Record-low interest rates during the pandemic dramatically increased borrowing power. But construction struggled to keep pace, constrained by factors including labour shortages, supply chain breakdowns, rising material costs and municipal rules. Then, as home prices spiked, interest rates also rose, and it became more expensive to borrow money. Many prospective homebuyers were shut out of the market.

In response the federal government made big promises. “An entire generation of young Canadians is questioning whether they can afford a place to live today and whether they will ever be able to own a home of their own,” states Ottawa’s 2024 housing plan, pledging 3.87 million new homes by 2031.

In 2025 prime minister Mark Carney announced Build Canada Homes, a new federal agency meant to scale up affordable home construction using public lands, funding tools and new building technologies. But a closer look at planned spending on housing programs, by the parliamentary budget officer, found little action to date on that promise. Federal spending will actually decline by 56 per cent in the next four years, and the government has not yet laid out an overall plan to achieve its goal to double the pace of housing construction over the next decade.

Even so, the market housing affordability problem is one that no single level of government can fully solve. As Mike Moffatt and Alex Beheshti, housing economists with the Missing Middle Initiative at the University of Ottawa, said in a December 2025 report, “While the federal government can and must do more, most housing policy levers rest with the provinces and municipalities.”

Governments can set the rules and offer incentives, adds Sandeep Agrawal, professor and inaugural director of the School of Urban and Regional Planning at the University of Alberta, but they don’t build most of the homes. “Someone can make all the policies… and they have some effect on the market,” he says. “But 50 per cent or more is in the hands of builders and developers and what people are looking for.”

In Canada, “housing affordability” typically refers to whether homeowners and renters can access housing that is reasonably priced relative to their income. Many governments use a simple definition: housing is “affordable” if it costs less than 30 per cent of household income before taxes. It’s a widely used but blunt tool.

For homeowners, housing costs typically include mortgage payments, property taxes, condominium fees and utilities. For renters, it’s rent and utility costs. That leaves out real-life expenses that add up, such as tenant or home insurance (which in Alberta is higher than the national average), maintenance costs for older homes, and transportation. A cheaper home on the city’s edge can quickly become costlier once fuel, parking and vehicle ownership are factored in. Some governments do account for this. Edmonton’s city plan, for instance, aims for households to spend no more than 35 per cent of average expenditures on housing and transportation combined. But most governments do not.

“Affordable housing,” meanwhile, is its own complex category. Many assume the term refers solely to government-subsidized rentals, but the Canada Mortgage and Housing Corporation (CMHC) defines it broadly, including housing provided by the private, public and non-profit sectors. In Alberta the provincial government’s 10-year affordable housing strategy, Stronger Foundations, released in 2021, focuses on new housing units and more rent supplements, aiming to serve 40 per cent more households. But Alberta is falling short of its goal, and experts caution that using subsidies to help make market housing more affordable can keep people in private rentals, which may not provide rent stability.

When it comes to market housing, Alberta has long been viewed as a relative bright spot—a place where homeownership, while harder than it once was, remains more attainable than in most of Canada. That reputation drew people. In 2022 the province launched its “Alberta is Calling” campaign to attract skilled workers with the promise of low taxes, comparatively cheaper homes and higher wages.

Around the same time, federal immigration changes contributed to unprecedented population growth across Canada, with the country’s population increasing by a record one million people in 2022 and, at the time, federal targets for bringing in newcomers set to rise year over year. By mid-2024, even Canada’s national housing agency conceded the country could no longer build its way back to 2004 affordability levels—a baseline year chosen because the economy was steady and housing costs were still proportionate to average incomes. CMHC instead shifted its target to 2019 levels, calling them more realistic.

In Alberta, a surge in both interprovincial and international migration in 2024 led Calgary and Edmonton to their biggest population growth in more than 20 years. People began “chasing affordability,” as ATB chief economist Mark Parsons put it in a report of the same name. Affordability issues, however, were felt unevenly across the province. A recent analysis by the parliamentary budget officer, for instance, found that Calgary saw a sharp deterioration in affordability compared to other major cities in Canada, while Edmonton remained among the most affordable.

In response, new home construction ramped up dramatically. Calgary led the country in housing starts in 2024 and was on track to repeat that in 2025. Edmonton hit an all-time high in 2024, surpassing a record that had stood since 1978. “The market’s largely been able to respond,” says Scott Fash, CEO at BILD Alberta, an association that represents builders and developers across the province. “But with housing, it can never respond at the speed at which growth often occurs. That’s the lag of going through approvals and then actually building the housing units.” A growing share of that construction is purpose-built rental, historically a small slice of Alberta’s housing starts. New CMHC incentives have rapidly increased builder enthusiasm; in 2025, purpose-built rentals accounted for 37 per cent of housing starts in the province. Still, inventory remains below 10-year averages, and prices remain above them. Fash’s organization also monitors markets outside Calgary and Edmonton, and has noted demand pick up in Grande Prairie, Red Deer and Lethbridge.

And while new builds add supply, experts warn more construction alone won’t fix affordability. The financialization of housing—treating homes and rental units as financial assets for profit, driven by large investors such as REITs, private equity and pension funds—continues to push prices higher. A report on the financialization of housing, for Canada’s independent federal housing advocate, describes it this way: “Financial firms operate rental housing with a goal to increase rents, making it their business model to reduce affordability.” About 20 to 30 per cent of Canada’s rental housing is now financialized, the Canadian Human Rights Commission estimates, which most impacts disadvantaged groups.

In Calgary, median home prices have risen dramatically—more than 40 per cent in the last five years.

It was into this landscape that Cass and Mike began searching. They set a budget of $650,000 to $800,000 and aimed to put 10 per cent down on a 30-year mortgage—without family assistance. They’d been saving for a down payment in a First Home Savings Account, a federal program launched in 2023 that lets first-time buyers put money tax-free into a down-payment account.

Like many first-time buyers, they faced the twin hurdles of saving enough for a down payment and qualifying for a mortgage—both of which have become harder in recent years. And because Mike is self-employed, they had to provide additional documentation to secure financing. It now takes a typical young Albertan about 10 years of full-time work to save a 20 per cent down payment, according to think tank Generation Squeeze. For Baby Boomers, it took roughly six.

Cass and Mike approached their purchase deliberately, wanting to ensure they could manage mortgage payments on a single income if necessary and avoid slipping into being house poor. “We didn’t want to get into a scenario where we bought a house and then all we could do was stay in our house,” Cass says. Their search unfolded alongside a stretch of declining interest rates, as the Bank of Canada cut its benchmark rate from 4.75 per cent in June 2024 to 2.25 per cent in October 2025, lowering borrowing costs and nudging more buyers back into the market.

That market was still challenging for first-time buyers. In Calgary, median home prices have risen dramatically—more than 40 per cent in the last five years—while median incomes have not kept pace. Reid Hendry, the City of Calgary’s chief housing officer, says the “price-to-income ratio” has been widening for decades. In 2000 the city had the “gold standard” level of “3:1 over an entire-market basis.” Now the city’s ratio is “approximately 5.5:1.” This means that compared to 2000 it now takes nearly double the amount of time—close to six years instead of three—for people making the average household income in Calgary to buy a home. “When we talk about affordability,” says Hendry, “we often focus immensely on price, but what’s very important as well is income.”

While Cass and Mike searched for an affordable home in Calgary, they might have had an easier time looking in Edmonton. A 2025 analysis pegs Edmonton’s price-to-income ratio at 4.61—the second-best among Canada’s 22 metro areas over 200,000 people (in that analysis, Calgary’s ratio is calculated as 6.14). “Edmonton consistently ranks as one of the most affordable large cities in Canada, despite having some pretty big population increases over the last couple of years,” says Travis Pawlyk, branch manager of development services for the City of Edmonton.

Why is that? Pawlyk frames the city’s role in supporting housing affordability as one of facilitating supply. The City has used policy and regulatory changes to encourage a diversity of housing types and speed up development permitting, letting developers respond quickly to market conditions. The Canadian Home Builders’ Association ranked Edmonton first among Canadian municipalities for its development processes, approval timelines and fees in its two most recent benchmarking studies.

A major policy piece is the city’s new zoning bylaw, introduced in January 2024. It allowed more housing types and higher density across the city, including up to eight units on lots previously restricted to single-family homes. While a significant rewrite, it built on years of prior reforms. “This is about a decade in the making,” Pawlyk says, echoing a sentiment shared widely. “Housing affordability doesn’t happen by accident,” wrote then-councillor and now mayor Andrew Knack in an Instagram post in April 2025. “It happens through deliberate policy decisions over a long period of time.”

The increase in housing supply “is largely due to reforms made by municipal governments, rather than by the government of Alberta.”

Major policy shifts began around 2015, Pawlyk notes. That year, Edmonton amended its zoning bylaw to allow subdivision of residential properties at least 50 feet wide. Secondary and backyard suites were also permitted on most single-family lots, and by late 2019, duplexes and semi-detached homes became permitted uses, effectively ending single-family-only zoning. In 2020 Edmonton became the first major Canadian city to eliminate parking minimums for homeowners and businesses entirely.

These changes have not come without pushback. “Edmonton neighbourhoods in revolt over residential lot-splitting,” read a 2016 Edmonton Journal headline. More recently, former Liberal leader and MLA Kevin Taft and other members of the Coalition for Better Infill criticized the 2024 bylaw for “deregulating the infill industry, eliminating most neighbourhood input and relaxing or removing many regulations.”

Still, Pawlyk emphasizes the need for Edmonton to grow differently, moving away from the long-standing assumption that new suburbs will absorb most population growth. Compact development, he says, advances both financial and sustainability goals, but it requires creating conditions for more residents in mature neighbourhoods—a shift he says takes political courage.

Federal funding has helped. Edmonton received $192-million through the Housing Accelerator Fund, some of which supports an Infill Infrastructure Fund to offset the cost of public infrastructure upgrades—a major barrier to building new homes in established areas, according to the city. Another federal measure eliminates the Goods and Services Tax (GST) for first-time buyers on new homes up to $1-million, offering direct relief to buyers.

Provincial initiatives to reduce impediments to building also played a role, though to what extent is up for debate. “While housing supply has been rapidly increasing in the province, that is largely due to reforms by municipal governments rather than the government of Alberta,” wrote housing economist Mike Moffat in a May 2025 report card that gave Alberta the lowest grade among the provinces for taking action to address housing supply. Calgary and Edmonton were singled out for leadership on zoning, approvals and permitting, with a recommendation that these best practices be applied province-wide. Edmonton also earned recognition for becoming the first Canadian city to institute an automated permit review system, reducing parts of the permitting timeline by 95 per cent or more.

In December 2025 Moffatt and the Missing Middle Initiative released a new report card that gave each province a grade based on several categories, including housing supply. Compared to the previous report card in May, Alberta’s score was up—tied for third overall—and the province got the highest score in the country in the category that asked: “Is the housing supply increasing, and are there enough homes to house the current population?”

Industry groups, meanwhile, are pushing for greater consistency across municipalities. Scott Fash with BILD Alberta says his organization recently consulted with municipalities, industry and the province to identify legislative changes that could streamline development further. A key priority, he says, is taking what works well in one place and replicating it more broadly. “We want to be able to create approval systems and zoning where we can go ahead and respond to the market in a pretty rapid fashion,” Fash says. “We’re better than most of the rest of the country, in terms of being able to do that quickly, but there’s still some work to be done.”

A three-storey multi-family home under construction in the Grovenor neighbourhood, Edmonton, February 2024.

Searching in Calgary, Cass and Mike wanted a single-family detached home built in the late ’80s or early ’90s, ideally in the northwest, close to family and within the ring road to keep commutes manageable. In August 2025 they found what they were looking for: a 1,700-square-foot, three-bedroom home in Scenic Acres, the same northwest Calgary neighbourhood Cass had lived in as a kid. The house, built in 1990, was mostly original, save for what Cass describes as a DIY kitchen facelift. It had a large yard, an attached front garage and the feel of a classic suburban family home. “It was one of the first places we had seen that we both felt confident in saying yes to,” Cass says. They viewed the house the first day it was listed and immediately put in an offer over the $674,900 asking price. Their bid was successful and they ultimately closed at $689,500.

When Cass and Mike bought their first home, in their late 30s, the moment landed with a mix of excitement and apprehension. It was, after all, the biggest purchase of their lives. “I never in a million years thought I would ever spend this much money in one fell swoop,” Cass says.

There was also a glaring way to put their purchase into perspective. Thirty-three years earlier, Cass’s parents had built a 1,350-square-foot bungalow on a corner lot in the same neighbourhood for $119,000. They were in their early 30s, raising two young kids on a single income. A generation later, prices in Calgary had climbed so dramatically that what was once attainable on one salary now typically requires two, many more years of saving and a bit of luck.

Near the end of 2025, as Cass and Mike were settling into their new home, conversations around housing began to shift again. Federal immigration policy had slowed international arrivals, though interprovincial migration into Alberta remained strong. Record-setting housing starts were beginning to catch up to demand, easing supply pressures and nudging prices down slightly from the previous year.

Still, chief housing officer Reid Hendry warned that momentum must be maintained. “The market has cooled a little, and home prices are quote-unquote softening, but what are they softening relative to?” he asked, stressing the need for continued government investment in meeting Calgarians’ housing needs. The nature of affordability challenges was shifting, now affecting a smaller slice of people but hitting that group more deeply.

For Cass, the day-to-day realities of homeownership were still sinking in, from needing to replace a broken fridge and adjust the surrounding cabinetry to make it fit, to being able to paint without asking a landlord’s permission. “More and more every week, it does seem more permanent,” she said. “And that’s a really nice feeling. It’s a lot less worrisome than thinking, ‘Are we going to have to move again next year?’ ”

Cailynn Klingbeil is a freelance writer and editor based in Calgary. Her articles have appeared in The New York Times, The Guardian and The Globe and Mail.

____________________________________________

Read More: Five Million Affordable Places to Live